Weigh before you pay: Debit or credit?

By Kathy Chu, USA TODAY

Among the debates that tend to vex shoppers — paper bags vs. plastic, plasma TVs vs. LCD — there's one standby: Credit or debit?

Weigh before you pay: Debit or credit?

By Kathy Chu, USA TODAY

Among the debates that tend to vex shoppers — paper bags vs. plastic, plasma TVs vs. LCD — there's one standby: Credit or debit?

The decision isn't a trivial one. When you shop, how you pay for your purchase can determine how much protection you'll have should the merchandise prove defective, how quickly you'll get your money back and whether you'll be digging yourself out of debt years later. Yet there's no one right answer for everyone. If you have the discipline to pay off your purchases on time each month, consider using your credit card, because you generally get more protection against faulty merchandise and fraud.

If, on the other hand, you tend to buy now and pay months later, you should stick to debit cards, cash or checks, because the money will come straight out of your bank account, sparing you interest charges. Just recognize that, even with debit cards, you could fall into debt if you're not careful. That's because banks are making it easier for you to overdraw and then charging you stiff fees for doing so. There's also the risk that fraudsters will steal your debit card. Typically, if debit card fraud occurs, you'll have less protection than with credit cards. That's why some consumer advocates suggest you use debit cards sparingly — if at all. "For a long time, people were saying, 'Use debit instead of credit,' " if you're debt-prone, says Ed Mierzwinski of the U.S. Public Interest Research Group. "But that thinking is shifting."

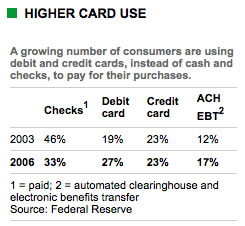

Still, both credit and debit have become ever-more-popular payment options. In 2006, for the first time, consumers paid for more purchases with debit and credit cards combined than with checks. Debit card use is growing especially fast; debit cards have surpassed credit cards as the most popular electronic payment, according to the Federal Reserve.

Before you pull out a debit or credit card, here's what you need to know:

Purchase protection and fraud

If whatever you buy proves defective, credit cards allow you to dispute the charges. Some debit cards do, too. But with debit cards, the benefits will vary by issuer, and sometimes depend on whether you signed for the purchase or instead entered a PIN. With a signature debit card transaction, "There are very defined rules about how defective merchandise would get handled, and you have rights you don't have with PIN," says Edward Kadletz, Wells Fargo's head of debit cards. Meanwhile, if fraudsters strike, you often have stronger protection with credit cards than with debit cards. With credit cards, under federal law, you're liable for no more than $50 if fraud occurs, though most issuers don't hold you liable for even that much. With debit cards, your maximum exposure is $50 if you report it within 48 hours. Report it after 2 days, and you could be liable for up to $500. Take longer than 60 days, and you could be responsible for the entire dollar amount of fraud.

Banks often provide more protection on debit card transactions than required by law. Yet there are always exceptions to banks' policies, says Travis Plunkett of the Consumer Federation of America, and those policies could change at any time. Major banks, including Bank of America, Citi,Wells Fargo and Chase, say that they'll credit consumers within a few days for fraud losses on debit cards, then investigate. At Wachovia, "if they've had other transactions where (there's been) fraud in the past, we will take that into consideration" in determining how quickly to credit the account for losses, says Chris Roberts, a senior vice president at the bank. Security experts say that if you use a debit card, you should sign for the purchase rather than enter a PIN. Why? Because while banks may offer zero liability for fraud that occurs with signature-debit transactions, they're often unclear about whether they'll provide equal coverage on PIN-debit card purchases, says Avivah Litan, a senior analyst at Gartner. Also, Litan warns, "If a thief steals your PIN, they can go to an ATM" and empty out your account.

Rewards

To encourage the use of credit and debit cards, banks offer points that can be redeemed for an array of rewards, including airline tickets, electronics and cash. Credit cards usually offer more lavish rewards than debit cards do. And among debit cards, PIN and signature transactions aren't created equal. Signing for a purchase often earns you more points than entering your PIN does. Citi's "ThankYou" rewards program generally offers up to five points for each dollar spent on a credit card. By contrast, it typically offers only one point for each $2 spent when you sign for a debit card purchase and one point for every $3 spent when you enter a PIN for a debit card sale. Other banks, including Chase and Wachovia, offer rewards on credit cards and signature debit transactions, but not on PIN-debit purchases. Why the uneven rewards structure? Banks usually make more money from processing a credit card than a debit card transaction. And banks earn more when you sign for your debit card purchase than when you enter a PIN.

Convenience and cost

One obvious reason for the growing popularity of credit and debit cards is that plastic is less cumbersome to carry around than a checkbook or a wad of cash. Using credit or debit cards also provides you with a record of where you're spending money, which can help with budgeting. Credit cards, of course, carry steep interest rates — especially for people with poor credit scores — and loads of fees. But if you have the discipline to pay off the card at the end of the month, you're essentially receiving an interest-free loan from the bank each month. "The challenge" with a credit card, says Chris Allen, a director at Hitachi Consulting, is that "you have to make sure you have enough money to pay it back." Debit cards also impose steep fees. And as more shoppers use debit cards for small-dollar transactions such as coffee and milk, banks are making it easier for consumers to trigger these fees. A few years ago, most banks denied a debit card purchase if you had insufficient funds. Not anymore. Today, most banks will approve even the smallest debit card purchase — then hit you with a fee of $35 or more. If you're going to use a debit card, sign up for low-cost overdraft protection. It will transfer money from your savings to your checking account if you overdraw. The fee for this service is often much less than the bank's fee if it automatically pays your overdraft.

There's also another option: "If you're really worried about (overdraft fees), then use cash," says Leslie Parrish, a senior researcher at the Center for Responsible Lending.